Almost every bank today calls itself digital. And by most measures, they are. Over the past decade, the industry has mastered the art of digital efficiency. Core systems have been modernized. Processes have been automated. Machine learning models have been deployed in pockets. Customers can transact faster, and operations run smoother.

Yet here is the uncomfortable truth for boards and CEOs: efficiency alone is no longer a differentiator. It is the cost of entry. Table stakes.

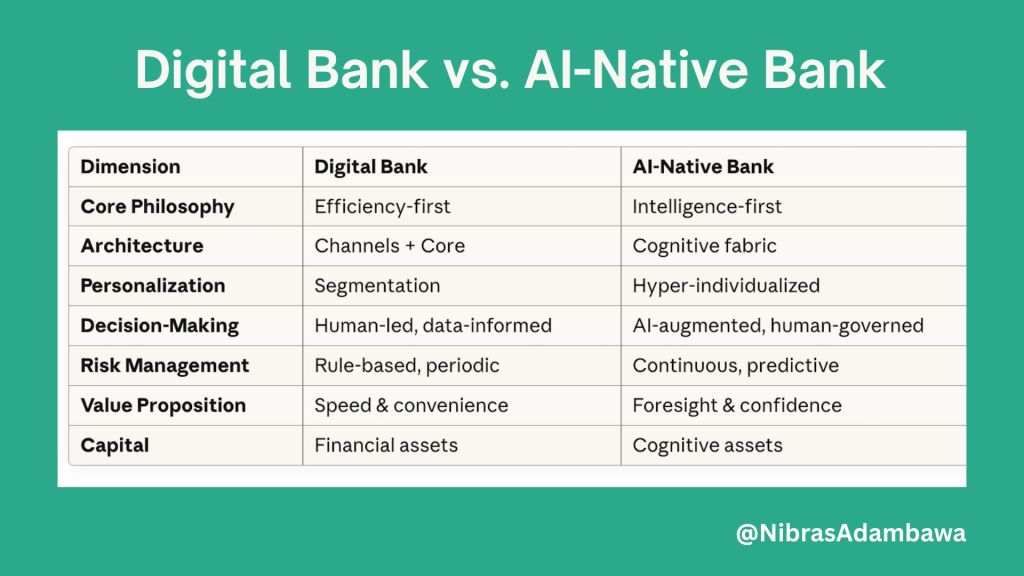

The real disruption is not about doing banking faster. It is about doing banking smarter. And that requires moving beyond digital-enabled banks to AI-native banks.

What It Means to Be AI-Native

Being AI-native is not about layering a few algorithms on top of legacy systems. It is not about having a data science team tucked inside operations or a “Center of AI Excellence” reporting into IT. AI-native means intelligence is embedded into the operating system of the bank. It becomes part of how the bank thinks, decides, and learns.

In an AI-native bank, every process – from credit underwriting to liquidity management, from risk modeling to compliance monitoring – learns and self-corrects. Decisions are continuously informed by data, models adapt dynamically, and outcomes are optimized in real time – all while remaining fully bounded by ethical, regulatory, and human guardrails.

In short, an AI-native bank doesn’t just use AI. It thinks in AI.

The Leadership Imperative

Achieving this is not a technology project. It is an organizational and cultural transformation. Boards and executive teams must confront a series of profound questions:

- How does intelligence flow across silos instead of merely automating them?

- How do models interact with governance, capital, and risk frameworks to improve outcomes without violating constraints?

- How do humans and machines co-create value, rather than seeing AI as a replacement for judgment?

The transition from digital-enabled to AI-native is not incremental. It is architectural, cultural, and strategic. Digital banks made banking faster; AI-native banks make banking smarter. It requires redesigning the very DNA of the institution, moving from managing information to managing intelligence.

From Delivery to Decision

Digital transformation was about delivery: faster transactions, more efficient operations, streamlined customer journeys. AI-native transformation is about decision: more precise, adaptive, and anticipatory judgment at every level of the bank. It is a shift from static policies to dynamic learning systems, from manual oversight to continuous, AI-augmented monitoring and insight.

Boards must recognize that AI-native banking is fundamentally about leadership. It demands a mindset willing to let intelligence reshape the core, not just support the periphery. The institutions that embrace this now will not merely keep pace – they will define the next era of financial services, setting new standards for trust, speed, and value.

The Real Questions

As we consider this evolution, the questions that matter for leadership are no longer about if or when AI should be adopted. The real questions are deeper:

Who in your organization is ready to let AI shape decisions, governance, and risk management? Are you prepared to redesign processes, roles, and metrics around intelligence rather than compliance checkboxes? Do your executives and board members understand what it means to measure value through insight, not throughput?

Technology alone will not make a bank AI-native. Talent alone will not. Mindset alone will not. It is the combination – and above all, leadership commitment – that will define success.

The choice is clear: banks can remain digital-enabled, competing on efficiency, or they can become AI-native, competing on intelligence. The difference is existential.

The question for every board, CEO, and executive committee is this: are you ready to rebuild your bank’s DNA around intelligence, or will the next generation of AI-native institutions define the rules without you?

See my other post on the same topic here